Private Wealth Management. AI-Driven Financial Guidance

End-to-end wealth management, powered by Quantel AI

Trusted by the executives of the TOP companies

Ask Quantel AI anything.

Try Quantel AI, book a call with an advisor, or schedule a meeting with us in person.

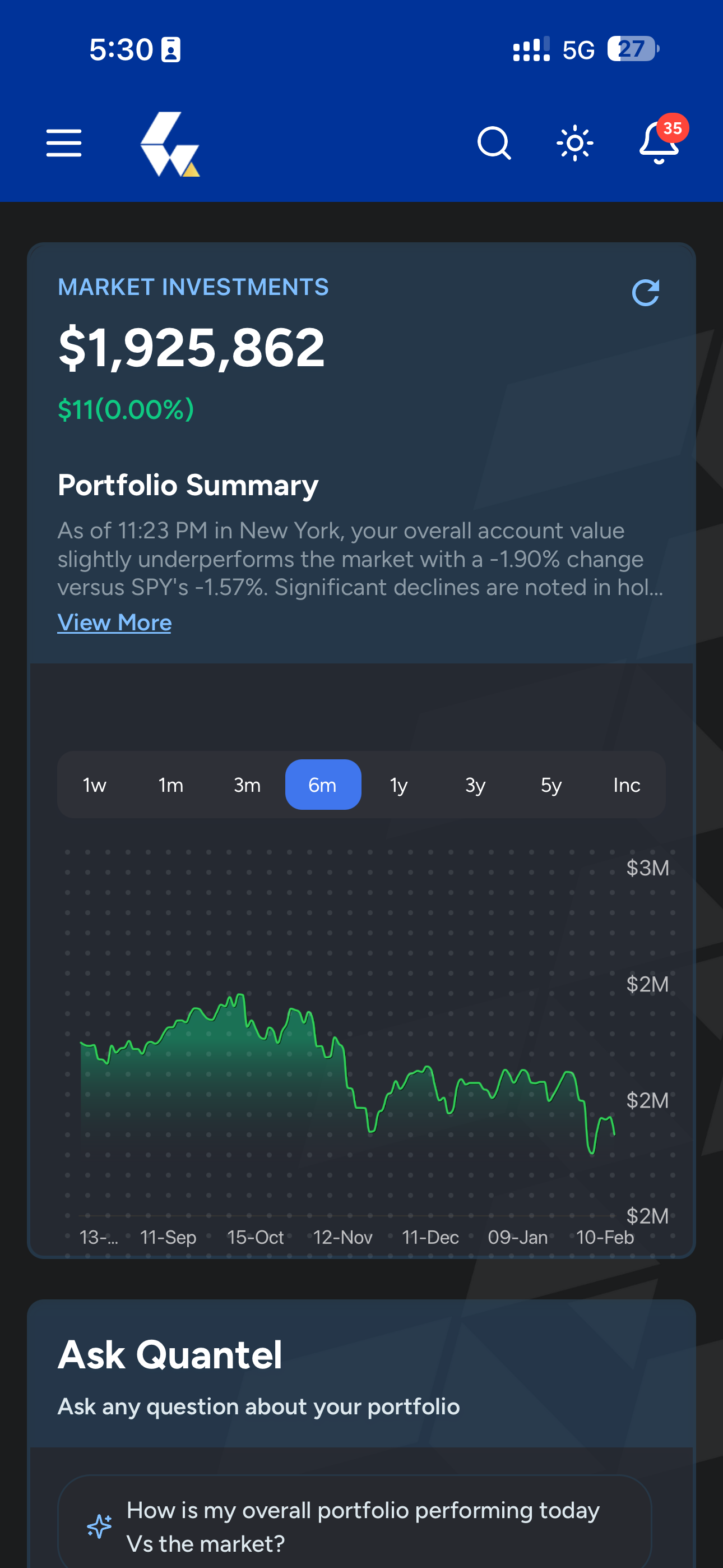

Investment Intelligence, Always on

Hear directly from clients and advisors leveraging data backed systematic investment strategies.

Vernon S

Senior Marketing Executive • Dubai, UAE

“The team has elevated my investment experience, making it completely stress-free. Their meticulous updates and transparency at every stage have earned my full trust.”

Pick your path to smarter wealth.

Explore our AI platform, investment solutions, advisory services, or family office support—no obligation.

You Set the Goals, Quantel Does the Work.

Tailor-made wealth management strategies, designed to align with your unique financial goals and risk tolerance.

Simulated returns. Figures shown are hypothetical illustrations only; actual results may vary widely based on market conditions, taxes, fees, timing, and other factors. Not a prediction, offer, or guarantee of future performance.

Quantel Invest

Goal projection · Illustrative

See your edge

Monthly amount, years, then Quantel vs. S&P—one glance, illustrative only.

Your Decisions, Quantel’s Expertise.

Systematic Guidance and Insights for Better Investment Decisions.

Quantel Advise

Linked accounts · Illustrative

Secure connections

Plaid

Banks, cards, loans & cash

Interactive Brokers

Investments & custodian

Built for clarity, not complexity.

Each step contrasts Quantel vs traditional wealth firms

with subtle motion and microdemos.

Monitoring & responsiveness

01

Quantel

Always-on monitoring with clear alerts. What changed, why it matters, and what to do next.

Traditional firms

Periodic reviews with limited real-time insight and slower reaction to market shifts

Investment process

02

Quantel

A documented, repeatable framework. Models, constraints, and rationale live in one system.

Traditional firms

Advisor – led approaches – variable, less consistent and harder to track.

Taxes & tradeoffs

03

Quantel

Tax impact modeled before action. So tradeoffs are explicit, quantified, and explainable.

Traditional firms

Taxes often considered after decisions are made, limiting after-tax optimization.

Transparency & trust

04

Quantel

Every portfolio change comes with a clear, concise explanation you can revisit anytime.

Traditional firms

Lengthy reports with limited clarity on why changes were made

Pricing

One system, three ways to work with Quantel.

Trust Quantel with full portfolio management. Or, if you prefer to stay in control, get personalized recommendations. Tailored to your account.

Pay-per-use help,

when it matters.

Engage a fiduciary for risk managed, account-aware recommendations.

You can also move to discretionary management when you're ready.

Quantel Advise

Fiduciary consultations, account-aware recommendations, and a written summary you can keep.

$149 / session (Free)

One-off clarity when you need it.

$99 / session (Pro)

Lower pricing when you're investing with Quantel.

$249 / month Advisory Pass

Ongoing access to your fiduciary team.

Advisory and investment management services provided by Quantel, an SEC-registered investment advisor.

Global Investors. U.S. Growth. Quantel Intelligence.

Quantel helps you navigate, diversify, and scale wealth through risk managed intelligent exposure to U.S. markets and beyond.

Download the Quantel app.

Bring an added layer of confidence to your advisor’s guidance with Quantel AI.

Scan the QR code on your phone to download the Quantel app.

Ready to review your portfolio?

Start free in minutes. Upgrade only when you're ready.

Frequently asked questions

Quick answers to common questions. Can't find what you need? Reach out.

We manage actively designed portfolios across public markets, alternatives, and structured opportunities. Our focus is disciplined growth with risk awareness — not speculative trading.

No. Portfolios may include equities, ETFs, structured notes, and select alternative opportunities such as private investments, depending on suitability and goals.

Traditional managers often rely on static allocation models. We actively manage portfolios with attention to risk, tax efficiency, and market conditions.

Yes. We manage retirement accounts, brokerage accounts, trusts, and other investment structures — coordinating them under one strategy.